I think that people who are investing in mortgage REITs are chasing dividend yields and ignoring the downside risk of lower earnings, dividend cuts, and the lower asset values. This article from Seeking Alpha contributor, Todd Johnson, embodies what I’m talking about. The article’s contents are indented and my comments should be aligned to the left (not indented).

An Interview With American Capital's Gary Kain

37 comments | October 11, 2011 | about: AGNC, includes: ANH, CIM, CMO, CYS, HTS, IVR, MFA, NLY, TWO

Notice that there is no explicit Federal guarantee. Besides, even if there was an explicit Federal guarantee that wouldn’t mean anything either. The US federal government is running near a $1.5 trillion annual budget deficit. The budget annual budget deficits will grow when the country lapses into another recession. There are deficits as far as the eye can see. The biggest ponzi schemes: Medicare, Social Security, and the FDIC are running in the red now. Don’t put your investment/savings faith in governments ability to perpetuate their ponzi schemes.

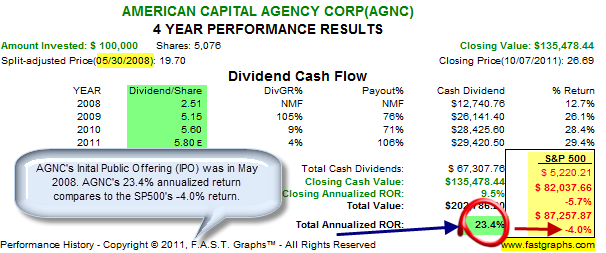

On Monday I had the fortunate experience to interview Gary Kain. Mr. Kain is the President and Chief Investment Officer of American Capital Agency Corporation (AGNC). American Capital Agency Corporation is a mortgage real estate investment trust (mREIT). American Capital Agency invests in only Government Sponsored Entity (GSE) mortgage backed securities (MBS), an agency-mREIT owns MBS which possess an implicit Federal guarantee. The stock currently pays a 21% dividend. The company has paid a quarterly $1.40-dividend, per share, for 9 consecutive quarters.

There are four new risks listed in the most recent 10Q statement. Each of them had further explanation that should raise your concerns.

· We have no employees and our Manager is responsible for making all of our investment decisions. Certain of our Manager’s officers are employees of American Capital and are not required to devote any specific amount of time to our business and each of them may provide their services to American Capital, its affiliates and sponsored investment vehicles, which could result in conflicts of interest.

· We may change our policies at any time without stockholder approval, including our investment policy, which may adversely affect our financial condition, results of operations, the market price of our common stock or our ability to pay dividends or distributions.

· Federal Reserve programs to purchase securities could have an adverse impact on the agency securities in which we invest.

· The market price of our common stock may fluctuate significantly.

Gary provided an enormous amount of information during the course of the interview. He answered every question I posed to him. I do not have his breadth of knowledge. Please visit the latest SEC 10Q for any issues which need clarification.

I would like to share my interview thoughts in this article. First, I would like to sincerely thank Gary Kain for taking the time for the interview. His professional attitude and industry knowledge were very impressive and illuminating.

Notice the dividend payout ratio at 106% estimated for the year 2011. This is a warning that AGNC will not be able to keep paying its $1.40 quarterly dividend with current earnings. This measurement of dividend safety will only get worse as AGNC issues new shares multiple times per year, to raise capital, to leverage 8x, to buy more agency securities.

click to enlarge

AGNC does not disclose which 26 counter parties it has agreements with. This is very opaque. Perhap they are doing business with AIG, Lehmen Bros., Bear Sterns, or some of the big European banks who foolishly leant money to the PIIGS (Portugal, Italy, Ireland, Greece, and Spain). We don’t know, but Gary Kain says, “Trust me.” Corporate executives are paid to lie. Do you need proof? Look at what any executive of a bankrupt company said before the bankruptcy. Enron’s Chairman, Ken Lay, is a good example that most people are familiar with. Counter parties can change the amount they are willing to lend in a moments notice. This is the modern bank run. Financial institutions are borrowed short and lent long. This is how Lehman Bros. went down so quick. Their lenders cut off their access to short term funding.

Liquidity Risk

My first question concerned liquidity risk. I asked if the Euro sovereign-debt could carry over to American Capital Agency's 26 counter parties. The counter parties provide liquidity for repurchase (repo) agreements. Gary confirmed this was not the case. In fact, counter parties have "increased lines" for repo agreements. Gary discussed this aspect with an example. If a counter party had a $1.5 billion lending line to the company, in some cases that has been raised to $2 billion.

If there is a rise in the one-month repo rate, the increase is likely to be limited to 5 basis points. At present time, the one-month repo rate is approximately 25 basis points.

The US is going back into recession. The unemployment rate is going to climb. More people will default on their mortgages. The GSE will have to guarantee the payments on the agency securities. There will be prepayments. This will hurt AGNC’s book value as some of the formerly prime MBSs become more toxic. Also, there will be prepayments from those who can refinance at historic low interest rates. This will be front page new in 3-6 months. I don’t think the GSE’s will break their promises until they run out of money. If the GSEs fail to guarantee the MBSs, then their book value will fall even more.

I watched the presentation that Gary Kain gave in September. He did a good job explaining the coming prepayment risk. Watch it here: http://wsw.com/webcast/jmp15/agnc/ . Of note is that 34% of AGNC’s portfolio are susceptible to high prepayment risks. At the end of his speech on slide 10 of his presentation he said, “Prepayment speeds are going to dominate our results [over the next six months].” You need to hope that the models are based on Keynesian economics. If they are, then the forward yield curves will be optimistically steep. If they are grounded in Austrian economics (this is unlikely), then the forward yield curves would be flat or inverting because of the coming recession. We read this at the bottom of page 7 in the latest 10Q report:

“We estimate long-term prepayment speeds using a third-party service and market data. The third-party service estimates prepayment speeds using models that incorporate the forward yield curve, current mortgage rates, current mortgage rates of the outstanding loans, loan age, volatility and other factors. We review the prepayment speeds estimated by the third-party service and compare the results to market consensus prepayment speeds, if available. We also consider historical prepayment speeds and current market conditions to validate the reasonableness of the prepayment speeds estimated by the third-party service and based on our Manager’s judgment we may make adjustments to their estimates. Actual and anticipated prepayment experience is reviewed quarterly and effective yields are recalculated when differences arise between the previously estimated future prepayments and the amounts actually received plus current anticipated future prepayments. If the actual and anticipated future prepayment experience differs from our prior estimate of prepayments, we are required to record an adjustment in the current period to the amortization or accretion of premiums and discounts for the cumulative difference in the effective yield through the reporting date.”

Prepayment Risk

This is the essential - and core aspect of the interview - area of focus. Gary reiterated this point on numerous accounts. He said, "In 3-6 months time, the focus will be on how we handled prepayment risk." American Capital Agency is clearly focused upon this issue. The company addressed this topic very clearly at the September 26th JMP Securities Financial Services and Real Estate Conference.

The company has focused upon owing GSE-MBS with the lowest prepayment risks. The GSE-MBS with the lowest prepayment risk include:

1. GSE-MBS with low balances,

2. GSE-MBS associated with the Federal Housing Finance Agency's (FHFA) Home Affordable Refinance Program (.pdf) (HARP).

The company, as of June 30th, has over 66% of its GSE-MBS portfolio invested in the two above categories. American Capital Agency was proactive in taking this stance prior to Federal intervention coming to page one of the Wall Street Journal. Gary reiterated during the course of the interview that AGNC's management and staff are focused upon maintaining or increasing American Capital Agency's book value per share. "We are not looking for any home runs in our book value", [but only to do our best to] "maintain or increase" [the book value per share].

If there is one key aspect this article should communicate is the impact of "prepayment risk".

Hedging Practices

I was curious to know if the company used "hedging" to only hedge its positions, or also to "speculate" on a high-probability event. Gary confirmed the company's hedging practices are designed to be agnostic towards the noise on the markets. His staff hedges the GSE-MBS to protect the book value per share. Gary wants to be able to walk into the office tomorrow and have a sound portfolio regardless if interest rates are "increasing or decreasing".

Gary commented, "we don't know how much is already priced in the markets. It's the same as with the stock market." My question resonated because I wanted to know if a high probability of "Operation Twist" (ie, the Fed selling short-term Treasury Bills and purchasing longer duration Treasury Bonds) was likely, would the company position themselves based upon this likelihood? The answer was "no". The focus is to be consistent and neutral on agency MBS price movement. Clearly, the company is focused upon protecting the book value and be a consistent performer.

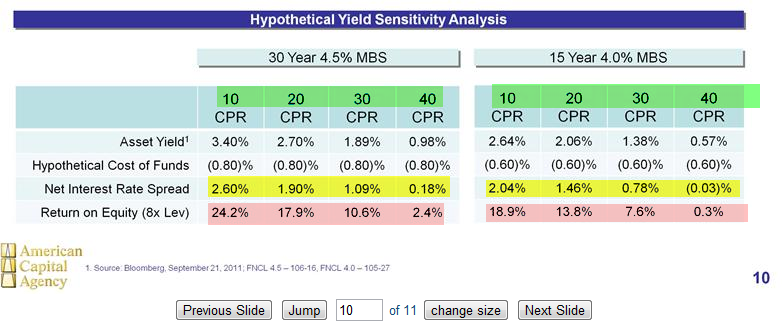

Gary took the time and patience of Job to explain the "hypothetical yield sensitivity analysis" for prepayment risk based upon the Constant Prepayment Rate (CPR), which is the percentage of principal that is prepaid over a period of time on an annualized basis. A couple of notes to highlight the prepayment risk:

· The highlighted "green" numbers reflect the percentage of prepayments in a given year,

· The highlighted "yellow" numbers reflect the net interest rate spread,

· The highlighted "salmon" numbers reflects the reflect on equity based upon an 8x leverage.

The key issue is Gary and American Capital have focused upon reducing the CPR a) to benefit the net yield spread, b) to benefit the return of equity, c) to benefit the book value per share, and d) to benefit the dividends for shareholders: "institutional and small". The company is 100% aligned with the goals of the common shareholder.

You might be asking yourself what constant repayment rate AGNC thinks they are going to experience in the near future. You should be asking yourself this because it greatly affect the company’s financial results. The answer lies on page 15 of the latest 10Q report. We read.

“The weighted average lives of the agency securities as of June 30, 2011 and December 31, 2010 incorporates anticipated future prepayment assumptions. As of June 30, 2011, our weighted average expected constant prepayment rate (“CPR”) over the remaining life of our aggregate investment portfolio is 10%.”

I believe this is overly optimistic.

Gary Kain used to work for Freddie Mac. You have to be Keynesian to work for a Government Sponsored Enterprise. Keynesians are leading the world off and economic cliff. Need I say more.

Benefits of Freddie Mac Experience

I asked Gary what benefits were gained by his extensive Federal Home Loan Mortgage Corporation (“Freddie Mac") work experience. There were some very intriguing responses on this issue.

· Gary's Freddie Mac experience required managing a "40 to 50x leveraged portfolio". This is in stark contrast to a current 8x leverage rate. He gained a greater "respect for hedging" when dealing with a high leverage rate.

· He learned how the GSE operates and thinks. Gary gained insight into the regulatory oversight as a GSE manager.

· Historically, mREITs traded GSE adjustable rate mortgages (ARMs). Gary's Freddie Mac experience was, historically, with both ARMs and fixed rate mortgages. It wasn't until much later did the publicly traded mREIT industry move more to the the fixed rate mortgage segment.

Leverage works both ways. Just ask Lehman Bros and Bear Stearns. More leverage will make mREITs a taller house of cards.

Will the mREIT Industry Expand its Leverage Rate

Presently, the agency-mREIT leverage rate is approximately 7x to 8x. This is historically lower than prior leverage rates. Gary believed the move, in the future, will offer opportunities to increase leverage. Presently, there are GSE unknowns which must sort themselves out.

GSEs will be shrinking in market size over the next 7 years. The ability to increase leverage levels upward from a 7x-leverage rate to higher levels clearly is an opportunity for the agency-mREITs once there is stability amongst the Euro sovereign debt, SEC 60-day review period, Fed Operation Twist, Treasury programs, and Policy Risk - HARP. Gary's focus is ignoring the noise and recognizing what truly matters. Time will pass and well-prepared companies will be at the center of attention.

This is expected. The profits that the current mREITs are generating are the signal to other entrepreneurs to enter the mREIT markets. More competition will bid up MBS prices all other things being equal. This will lower profits at the existing mREITs. What bothers me is that this is an artificially lucrative market caused by perceived government guarantees of MBS. That means that capital will be misallocated. Someday there will be a bust when the next financial crisis hits.

Backlog of mREIT IPOs

I wanted to know Gary's thoughts on the backlog of mREIT initial public offerings. The SEC is asking for feedback on a couple of issues:

·

o The SEC, as of August 31st, is seeking "Public Comment on Asset-Backed Issuers and Mortgage-Related Pools Under Investment Company Act".

o The SEC, as of August 31st, is seeking under a separate concept release, public comment on "interpretations of a provision in the Investment Company Act – Section 3(c)(5)(C) – that may be used by some companies engaged in the business of acquiring mortgages and mortgage-related instruments such as some REITs".

Agency mREITs provide a fluid buy and sell marketplace for the $10 trillion mREIT sector. There are, however, a few companies who are interested in entering this sector. It is important to note the difference between a non-agency mREIT and an agency mREIT. Agency mREITs own only GSE-MBS implicitly backed by the U.S. Federal government.

One of the companies who is interested is Pimco. Pimco's "Bill Gross" is almost synonymous with the word "bond". He has certainly gained a following over the years. Pimco would like to enter the mREIT sector, per its April 5th filing.

My bet is with Benjamin Graham and Austrian economics. Graham recommended that average investors should not own financial stocks and insurance stocks because you don’t know what is really going on in those companies from their reporting. The Austrian school teaches that central banks cause the boom-bust cycle. The Federal Reserve’s actions caused the financial crisis of 2008 and they are also the source of the coming crisis in 2011-2012. Keynesians predict that the stimulus will get economies out of recession, but the stimulus has noticeably failed. The Austrians predict that stimulus makes things worse.

In full disclosure, Jeffrey Gundlach, chief executive of DoubleLine Capital LLC and a veteran of more than 20 years in the industry, said in August he was passing on the mREIT sector. Mr. Gunlach recently discussed his desire for absolute returns instead of political ambitions. Mr. Gunlach stated to the Wall Street Journal, "I'm too old to raise money then go around the world and apologize," he said. Time will tell who had the insights and knowledge to prepare accordingly. On the agency mREIT sector, my bet is with Gary and American Capital.

Gary said as the GSEs exit the market place over the coming 7 years, there will be ample room for new mREITs to enter into the $10 trillion market place. The annual GSE MBS exit will result in shrinkage amounts of "$150 million to $200 million per year".

Summary

He calls at least 34% very little exposure. That is laughable. Operation Twist will make things worse for AGNC. So will the next FED operation after Twist, and the next one, and the next one after that. The Keynesians all think the next stimulus is the one that will work. This is nonsense.

American Capital Agency has very little exposure to GSE-MBS with "high prepayment risks". Management is cognizant of this risk and addressed the risks before Fed Chairman Bernanke came in with Operation Twist and CNBC had the topic as headline news.

I concluded the interview with complete confidence in Gary Kain's leadership and industry expertise. Gary was willing to discuss the challenges, opportunities, and unknowns. American Capital Agency has a leader to tackle any Federal government action, interest rate move, and prepayment risk in the best interests of shareholders.

Know the real risks of owning AGNC stock before you buy it. To read all my critiques of AGNC click here: http://www.myhighdividendstocks.com/category/high-dividend-stocks/american-capital-agency-corp

I believe the interview provides insights on the rewards of owning AGNC stock. The company has produced industry-best returns. The company is aligned with achieving a solid book value per share, dealing with the political and Euro sovereign-debt issue, and provide outstanding absolute positive shareholder returns. What more could a common shareholder desire?

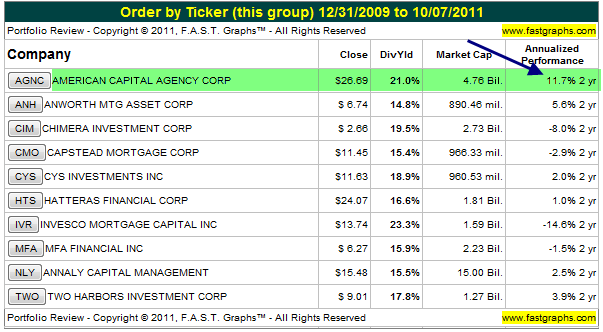

mREIT-Sector Peer Comparison

For background purposes, directly blow is a table showing the mREIT sector's financial performance. The chart assumes dividends are not reinvested. The dividends are assumed to be kept in cash.

Disclosure: I am long AGNC, CMO, CYS, HTS, NLY, TWO.

I don’t own AGNC or any other financial stock.

Link to the original Seeking Alpha article: http://seekingalpha.com/article/298768-an-interview-with-american-capital-s-gary-kain

Subscribe today for free at www.myhighdividendstocks.com/feed to discover high dividend stocks with earning power and strong balance sheets.

Be seeing you!

No comments:

Post a Comment